The relationship between cryptocurrency and traditional finance is evolving rapidly. What began as an alternative financial movement centered around decentralized assets is now increasingly merging with institutional banking, lending, and financial infrastructure.

- Why Bitcoin Is Increasingly Being Treated as Financial Infrastructure

- How Bitcoin-Backed Mortgages Work

- Why Avoiding Forced Bitcoin Sales Matters

- The Difference Between DeFi Lending and Mortgage Infrastructure

- Why Institutions Are Moving Toward Crypto-Backed Finance

- Why This Could Matter for the Housing Market

- Risks and Challenges Still Exist

- What Could Happen Next?

- Final Thoughts

- FAQ

One of the clearest signs of this transformation is the emergence of Bitcoin-backed mortgage products that allow borrowers to access home financing without selling their crypto holdings.

A new lending model introduced through collaboration between Coinbase and Better Mortgage is bringing this concept closer to mainstream adoption. The structure allows users to pledge Bitcoin as collateral while securing fiat-based mortgage financing through a regulated framework tied to traditional mortgage systems.

This development reflects a broader shift in how digital assets are being integrated into real-world financial infrastructure.

Why Bitcoin Is Increasingly Being Treated as Financial Infrastructure

For years, Bitcoin was primarily viewed as:

- a speculative investment

- a volatile trading asset

- an alternative monetary system

However, institutional adoption has significantly changed that narrative.

Bitcoin is now increasingly being discussed within the context of:

- collateralized lending

- treasury management

- financial infrastructure

- institutional reserves

- decentralized settlement systems

Growing discussions around Bitcoin’s role in cybersecurity infrastructure are also reshaping how governments and institutions evaluate decentralized networks.

This broader institutional recognition is helping transform Bitcoin from a speculative asset into a more functional component of modern finance.

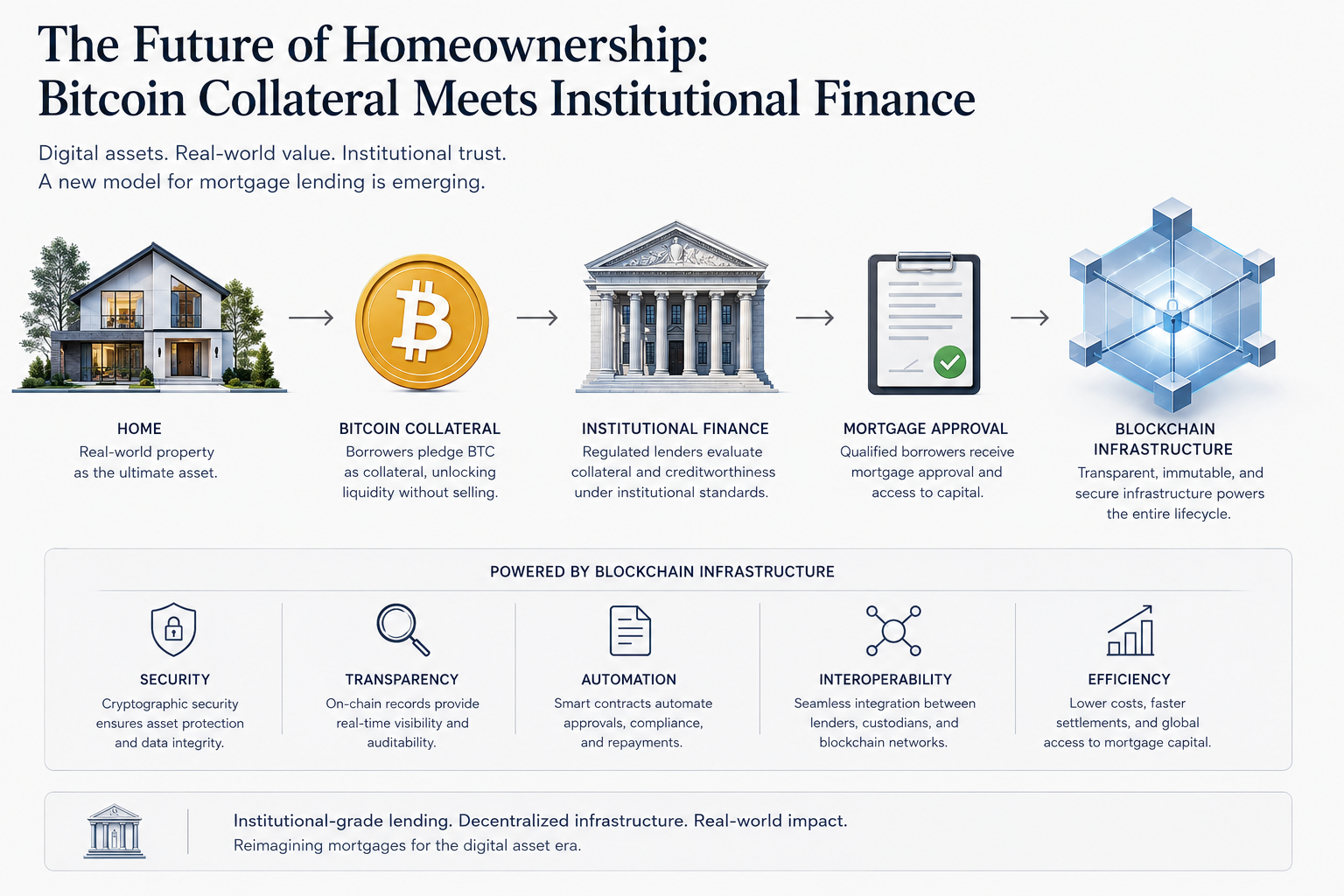

How Bitcoin-Backed Mortgages Work

The new mortgage structure allows borrowers to use Bitcoin as collateral while receiving a traditional fiat mortgage loan.

Instead of liquidating their holdings to fund a property purchase, borrowers can:

- lock BTC in custody

- maintain market exposure

- secure home financing

- access liquidity without triggering a sale

This creates a major difference compared to traditional crypto liquidation models.

The structure also reportedly aligns with frameworks connected to Fannie Mae, allowing these loans to integrate into broader mortgage infrastructure systems.

This is important because it moves crypto-backed lending closer to regulated financial markets rather than isolated DeFi environments.

Why Avoiding Forced Bitcoin Sales Matters

One of the biggest long-term concerns for crypto holders has been the need to sell assets to access liquidity.

Selling Bitcoin often creates:

- taxable events

- reduced long-term exposure

- missed upside potential

- portfolio disruption

Bitcoin-backed mortgages attempt to solve this problem by allowing holders to retain ownership exposure while using their assets as collateral.

For long-term investors, this model may provide:

- capital efficiency

- tax flexibility

- liquidity access

- portfolio continuity

As digital assets become more integrated into financial systems, collateral-based crypto lending models may become increasingly common.

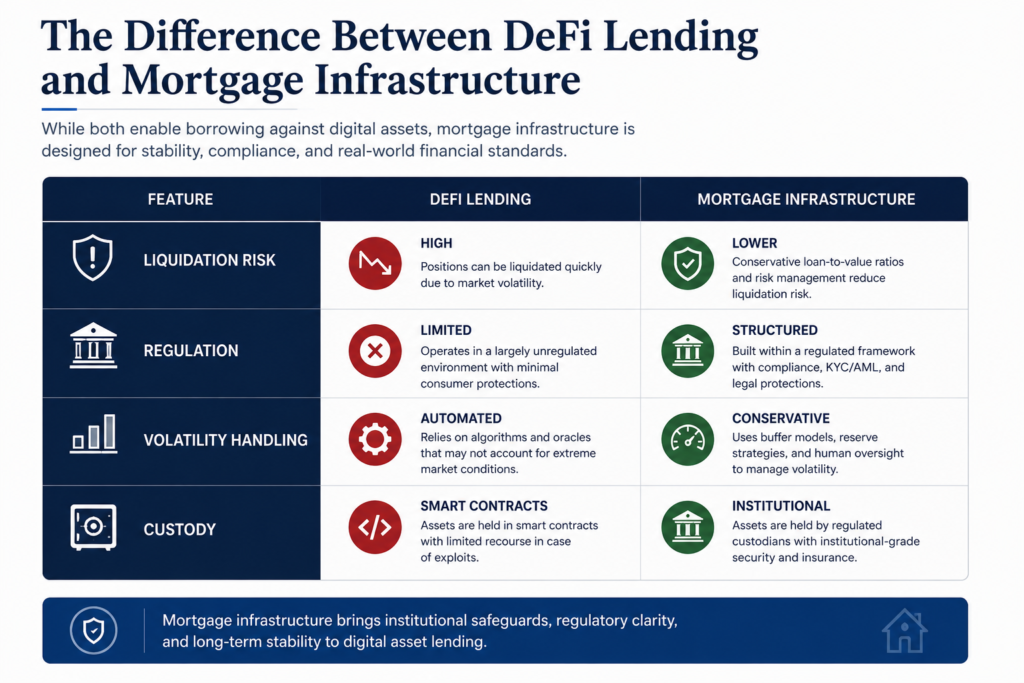

The Difference Between DeFi Lending and Mortgage Infrastructure

Traditional DeFi lending platforms often operate using automated liquidation systems.

If collateral values fall below required thresholds:

- assets can be liquidated automatically

- borrowers may lose positions quickly

- volatility can trigger cascading sell-offs

This has historically been one of the biggest risks associated with crypto-backed borrowing.

The newer mortgage-based model appears designed differently.

Rather than functioning purely through automated DeFi mechanics, the structure introduces:

- conservative lending ratios

- institutional oversight

- regulated custody systems

- traditional mortgage risk frameworks

This could reduce some of the volatility risks commonly associated with decentralized crypto lending.

However, risk still remains.

The broader blockchain industry continues facing major digital asset infrastructure risks tied to volatility, regulation, and financial stability:

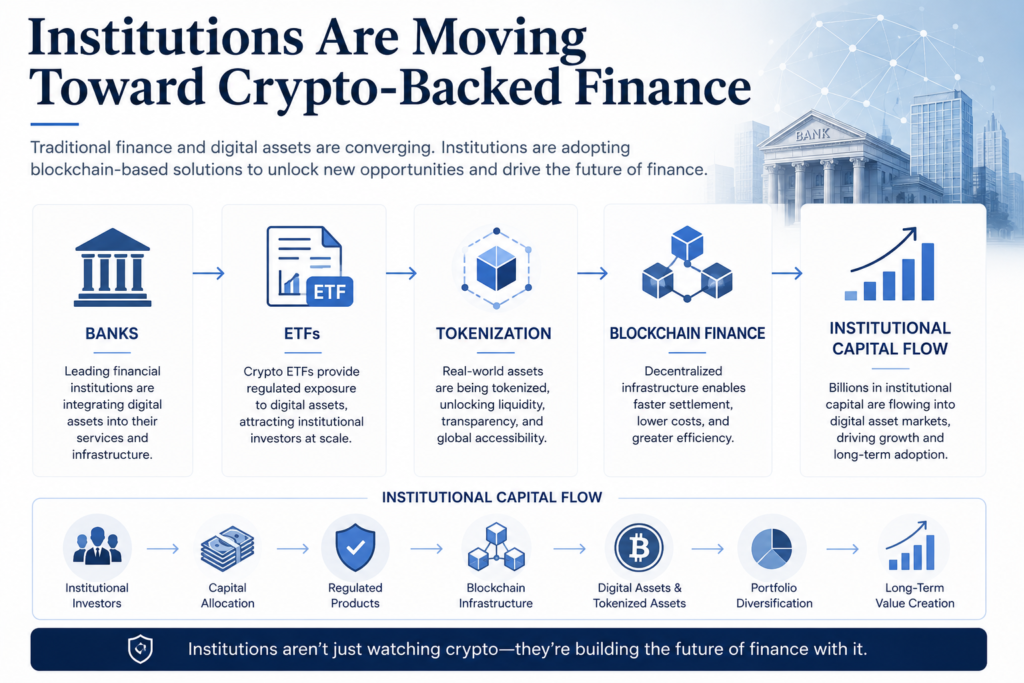

Why Institutions Are Moving Toward Crypto-Backed Finance

Institutional interest in blockchain infrastructure has expanded significantly over recent years.

Major financial firms are increasingly exploring:

- tokenized assets

- blockchain settlements

- crypto custody

- stablecoin systems

- decentralized infrastructure

- collateralized lending

This broader movement toward institutional blockchain adoption is changing how traditional finance interacts with digital assets:

Bitcoin-backed mortgages are part of this larger trend where crypto is transitioning from speculative trading into integrated financial infrastructure.

As institutional participation grows, more regulated crypto-finance products may emerge across:

- lending

- insurance

- settlements

- real estate

- payments

- treasury systems

Why This Could Matter for the Housing Market

Although still early, crypto-backed mortgage models could eventually influence how property financing operates globally.

Potential long-term impacts include:

- increased financial flexibility for crypto holders

- alternative collateral structures

- greater digital asset legitimacy

- integration of blockchain wealth into traditional banking

For younger investors who accumulated wealth through digital assets, these products may create pathways into real estate ownership without requiring full liquidation of crypto portfolios.

This is particularly relevant as more individuals hold significant portions of wealth in digital assets rather than traditional investment vehicles.

Risks and Challenges Still Exist

Despite the innovation, Bitcoin-backed mortgages also introduce several important risks.

Volatility Risk

Bitcoin remains highly volatile compared to traditional collateral assets.

Large market swings could still create:

- collateral pressure

- lending instability

- risk management challenges

Regulatory Uncertainty

Governments worldwide are still developing frameworks surrounding:

- crypto lending

- custody rules

- digital asset taxation

- mortgage regulation

- financial compliance

Future policy changes may significantly impact adoption.

Custody and Security Risks

Crypto-backed financial systems depend heavily on secure custody infrastructure.

The broader Web3 ecosystem continues facing serious DeFi security risks and cybersecurity challenges:

As institutional crypto lending expands, cybersecurity standards will likely become even more important.

The Bigger Shift: Crypto Is Becoming Financial Infrastructure

The most important takeaway may not be the mortgage product itself.

Instead, it is what the product represents.

Bitcoin is gradually evolving from:

- speculative digital asset

into:

- financial collateral

- infrastructure layer

- institutional reserve asset

- integrated banking component

This transformation reflects a much larger convergence between:

- traditional finance

- blockchain infrastructure

- institutional capital

- digital asset systems

The boundaries between Web2 finance and Web3 infrastructure are becoming increasingly blurred.

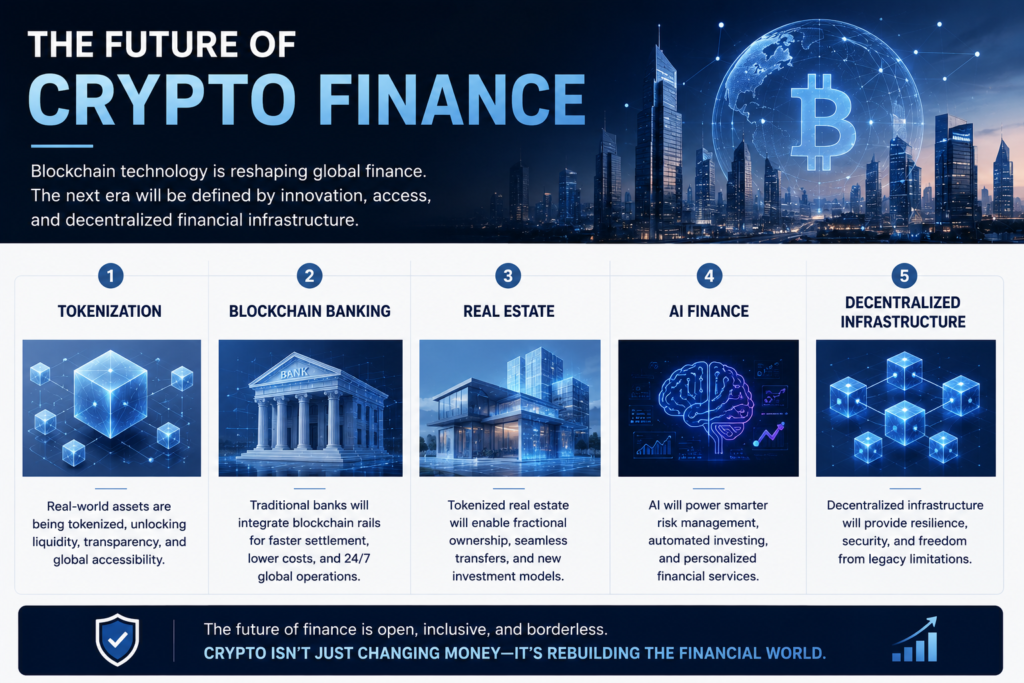

What Could Happen Next?

If Bitcoin-backed mortgage systems gain traction, future financial products could include:

- crypto-backed business loans

- tokenized real estate lending

- blockchain-integrated banking systems

- crypto collateral credit lines

- decentralized mortgage infrastructure

At the same time, advances in smart contract security systems and AI-assisted blockchain auditing may also improve trust in financial infrastructure built on decentralized networks:

The long-term success of crypto-backed finance will likely depend on:

- regulation

- infrastructure maturity

- institutional trust

- security standards

- market stability

Final Thoughts

Bitcoin-backed mortgages represent one of the clearest examples of cryptocurrency integrating directly into traditional financial systems.

Rather than forcing investors to choose between liquidity and long-term ownership, these lending models attempt to create a hybrid framework where digital assets can function as productive collateral within regulated finance.

While challenges surrounding volatility, regulation, and custody still remain, the broader direction of the industry is becoming increasingly clear:

digital assets are evolving into financial infrastructure.

As institutions continue expanding their involvement in blockchain systems, products like crypto-backed mortgages may become an increasingly important part of the future financial landscape.

FAQ

What is a Bitcoin-backed mortgage?

A Bitcoin-backed mortgage allows borrowers to use Bitcoin as collateral while receiving a traditional fiat mortgage loan.

Do borrowers need to sell Bitcoin for these mortgages?

No. The structure is designed to allow borrowers to maintain Bitcoin exposure while accessing financing.

Are Bitcoin-backed mortgages risky?

Yes. Bitcoin volatility, regulatory uncertainty, and collateral management remain important risks.

Why are institutions exploring crypto-backed finance?

Institutions are increasingly exploring blockchain infrastructure, tokenization, and digital asset integration within traditional financial systems.

Could crypto-backed lending become more common?

If infrastructure and regulation continue improving, crypto-backed lending products may expand across mortgages, business lending, and financial services.