Stablecoins are rapidly evolving from crypto trading tools into foundational infrastructure for the global financial system. What began as a mechanism for moving liquidity across cryptocurrency exchanges is now becoming a major component of:

- What Are Stablecoins?

- Why Traditional Global Payments Remain Inefficient

- Why Stablecoins Are Attractive for Payments

- How Stablecoins Are Expanding Beyond Crypto Trading

- Why Institutions Are Paying Attention to Stablecoins

- Stablecoins and Tokenized Finance

- Why Stablecoin Regulation Is Becoming a Global Focus

- Why Stablecoin Infrastructure Matters for Emerging Markets

- Why Security Remains Critical for Stablecoin Infrastructure

- Could Stablecoins Eventually Compete With Traditional Banking Rails?

- Final Thoughts

- FAQ

- cross-border payments

- remittance systems

- treasury operations

- settlement infrastructure

- digital commerce

- institutional finance

Governments, banks, payment providers, fintech firms, and blockchain companies are increasingly exploring how stablecoin networks can modernize global payments by enabling:

- faster settlement

- lower transaction costs

- programmable transactions

- 24/7 financial operations

- borderless value transfer

As adoption accelerates, stablecoin infrastructure is beginning to challenge some of the limitations of traditional payment systems built around banking networks and legacy settlement rails.

The future of digital payments may increasingly depend on how effectively stablecoins integrate with global financial infrastructure.

What Are Stablecoins?

Stablecoins are blockchain-based digital assets designed to maintain relatively stable value by being linked to external assets such as:

- fiat currencies

- treasury reserves

- commodities

- algorithmic stabilization systems

The most common stablecoins are pegged to the U.S. dollar.

Popular examples include:

- USDT

- USDC

- DAI

- FDUSD

Unlike highly volatile cryptocurrencies such as Bitcoin or Ethereum, stablecoins are designed to reduce price fluctuations while maintaining blockchain-based transferability.

This combination of:

- price stability

- instant settlement

- global accessibility

makes stablecoins particularly useful for payment infrastructure.

Growing institutional discussions around tokenized financial infrastructure are increasingly positioning stablecoins as a foundational layer of digital finance:

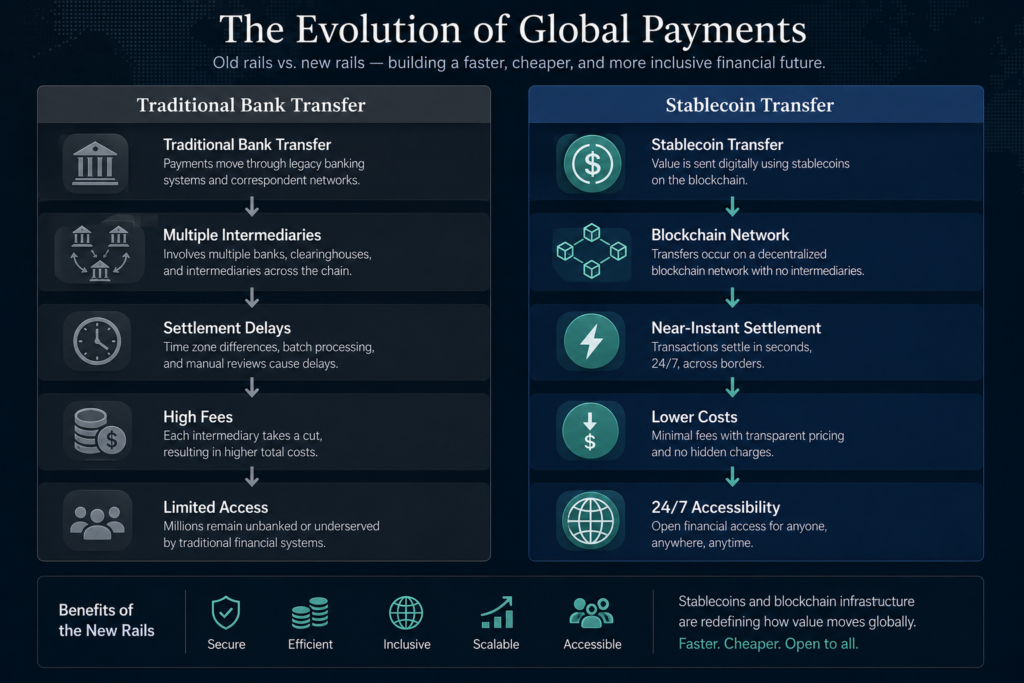

Why Traditional Global Payments Remain Inefficient

Despite decades of technological progress, global payment infrastructure still faces several major limitations.

Cross-border transactions often involve:

- multiple intermediaries

- settlement delays

- currency conversion costs

- banking restrictions

- limited operating hours

International transfers can sometimes take:

- several days

- complex compliance reviews

- expensive processing fees

Traditional systems such as SWIFT remain highly dependent on fragmented banking relationships and centralized settlement structures.

For individuals and businesses operating globally, these inefficiencies create:

- operational friction

- delayed liquidity

- higher costs

- accessibility barriers

Stablecoin infrastructure is increasingly being explored as an alternative settlement layer capable of reducing many of these constraints.

Why Stablecoins Are Attractive for Payments

Stablecoins combine several characteristics that make them highly attractive for digital payments.

Near-Instant Settlement

Traditional bank transfers may require multiple business days for settlement.

Stablecoin transfers can often settle within:

- seconds

- minutes

- continuously across global markets

This allows businesses and users to move value significantly faster.

24/7 Payment Infrastructure

Traditional financial systems typically operate within:

- banking hours

- settlement windows

- regional business schedules

Blockchain networks operate continuously.

Stablecoins enable:

- always-on payments

- weekend transactions

- real-time settlement

- global financial accessibility

Lower Transaction Costs

Cross-border payment systems often involve:

- correspondent banking fees

- wire transfer costs

- foreign exchange charges

Stablecoin transfers can reduce many of these expenses, especially for:

- remittances

- international commerce

- global freelancers

- digital businesses

Programmable Transactions

Stablecoin infrastructure can integrate directly with:

- smart contracts

- automated settlements

- treasury systems

- DeFi applications

- tokenized financial products

This programmability creates entirely new possibilities for financial automation.

How Stablecoins Are Expanding Beyond Crypto Trading

Initially, stablecoins were primarily used inside cryptocurrency markets to:

- move exchange liquidity

- hedge volatility

- facilitate trading

Today, their role is expanding rapidly.

Stablecoins are increasingly being used for:

- international business payments

- remittances

- payroll systems

- treasury management

- merchant settlements

- institutional transfers

In many emerging markets, stablecoins are also becoming alternative tools for:

- dollar access

- inflation protection

- cross-border savings

- digital commerce

This broader utility is helping transform stablecoins from speculative crypto tools into real-world payment infrastructure.

Why Institutions Are Paying Attention to Stablecoins

Large financial institutions are increasingly exploring stablecoin systems because of their potential to modernize settlement infrastructure.

Banks and payment providers are researching how stablecoins could improve:

- cross-border settlements

- liquidity management

- collateral mobility

- treasury efficiency

- financial interoperability

At the same time, governments and regulators are examining how stablecoins may impact:

- monetary policy

- banking systems

- financial stability

- capital controls

The rise of stablecoin infrastructure reflects a broader institutional movement toward blockchain-based financial systems.

rowing discussions surrounding institutional blockchain adoption demonstrate how digital asset infrastructure is gradually converging with traditional finance:

Stablecoins and Tokenized Finance

Stablecoins are becoming deeply integrated into tokenized financial systems.

They increasingly serve as:

- settlement assets

- collateral instruments

- liquidity layers

- trading pairs

- payment rails

As tokenized assets expand across:

- bonds

- treasuries

- real estate

- ETFs

- digital securities

stablecoins may become one of the core settlement mechanisms connecting blockchain infrastructure with traditional financial markets.

However, this integration also introduces systemic risks.

Growing concerns around tokenized finance risks show how stablecoin instability could potentially impact broader blockchain financial infrastructure:

Why Stablecoin Regulation Is Becoming a Global Focus

As stablecoin adoption accelerates, regulators worldwide are increasing scrutiny around:

- reserve transparency

- redemption rights

- liquidity management

- consumer protections

- systemic risk

One of the largest concerns involves whether stablecoin issuers maintain sufficient reserves during periods of market stress.

Large-scale redemption events could create pressure similar to:

- bank runs

- liquidity crises

- market contagion

This is especially important because stablecoins increasingly operate as core infrastructure across digital asset markets.

Governments are now exploring:

- licensing frameworks

- reserve requirements

- auditing standards

- stablecoin oversight mechanisms

The future growth of stablecoins will likely depend heavily on regulatory clarity and institutional trust.

Why Stablecoin Infrastructure Matters for Emerging Markets

Stablecoins may have particularly strong impact in emerging economies where:

- local currencies face instability

- banking access is limited

- remittance costs remain high

- cross-border payments are inefficient

In these environments, stablecoins can provide:

- faster international transfers

- digital dollar access

- lower transaction costs

- alternative financial rails

For freelancers, global workers, and digital businesses, stablecoins increasingly function as practical financial infrastructure rather than speculative assets.

This is one reason why stablecoin adoption is growing rapidly across:

- Latin America

- Africa

- Southeast Asia

- high-inflation economies

Why Security Remains Critical for Stablecoin Infrastructure

As stablecoins become more integrated into financial systems, infrastructure security becomes increasingly important.

Stablecoin ecosystems rely heavily on:

- smart contracts

- blockchain networks

- custody systems

- reserve management

- operational infrastructure

The broader blockchain industry continues facing major DeFi security risks tied to:

- smart contract exploits

- bridge vulnerabilities

- liquidity attacks

- governance failures

Modern smart contract security systems are increasingly integrating AI-assisted auditing and automated vulnerability detection to improve payment infrastructure resilience.

Without strong security systems, stablecoin infrastructure may struggle to achieve mainstream institutional adoption.

Could Stablecoins Eventually Compete With Traditional Banking Rails?

One of the biggest long-term questions involves whether stablecoins could eventually compete directly with traditional payment infrastructure.

Stablecoins already offer advantages in:

- speed

- accessibility

- programmability

- global reach

However, traditional financial systems still dominate in:

- regulatory integration

- consumer protections

- banking relationships

- compliance infrastructure

Rather than fully replacing banks, stablecoins may ultimately evolve into:

- hybrid financial infrastructure

- blockchain settlement layers

- interoperable payment systems

The future of global payments may involve increasing collaboration between:

- banks

- fintech firms

- blockchain networks

- stablecoin issuers

- regulators

Final Thoughts

Stablecoins are rapidly evolving into one of the most important infrastructure layers within the digital financial ecosystem.

What began as a crypto-native liquidity tool is increasingly becoming:

- cross-border payment infrastructure

- institutional settlement technology

- programmable financial rails

- tokenized economy infrastructure

Their ability to combine:

- blockchain efficiency

- digital accessibility

- price stability

- programmable settlement

positions stablecoins as a major force shaping the future of global payments.

However, large-scale adoption will depend heavily on:

- regulation

- infrastructure security

- reserve transparency

- institutional trust

- operational resilience

As blockchain systems continue integrating with global finance, stablecoins may become one of the clearest examples of how Web3 infrastructure transforms real-world economic activity.

FAQ

What are stablecoins?

Stablecoins are blockchain-based digital assets designed to maintain stable value by being linked to external assets such as fiat currencies.

Why are stablecoins important for payments?

Stablecoins enable faster settlement, lower costs, 24/7 transfers, and programmable financial transactions across blockchain networks.

How are stablecoins used in global payments?

Stablecoins are increasingly used for remittances, cross-border commerce, payroll systems, treasury operations, and institutional settlements.

What are the risks of stablecoin infrastructure?

Major risks include reserve instability, liquidity pressure, smart contract vulnerabilities, regulatory uncertainty, and cybersecurity threats.

Can stablecoins replace traditional banking systems?

Stablecoins may not fully replace banks, but they could become an important settlement layer within future hybrid financial infrastructure systems.