Tokenization is rapidly becoming one of the most important developments in modern financial infrastructure. What began as an experimental blockchain concept is now attracting attention from:

- What Is Tokenized Finance?

- Why Financial Institutions Are Interested in Tokenization

- Why the IMF Is Concerned About Tokenized Finance

- Instant Settlement Could Accelerate Market Crashes

- Stablecoins Could Become a Major Structural Risk

- “Code Is Law” vs Financial Stability

- Why Governments and Central Banks Are Paying Attention

- Why Smart Contract Security Matters in Tokenized Finance

- The Future of Tokenized Financial Infrastructure

- Final Thoughts

- FAQ

- global banks

- asset managers

- governments

- central banks

- fintech companies

- institutional investors

Financial institutions are increasingly exploring how traditional assets such as:

- stocks

- bonds

- real estate

- treasury products

- commodities

can be converted into blockchain-based digital tokens.

Supporters argue that tokenization could modernize financial markets by improving:

- settlement speed

- transparency

- liquidity

- operational efficiency

- global accessibility

However, growing concerns are also emerging around the risks associated with highly automated and interconnected blockchain financial systems.

The International Monetary Fund (IMF) has warned that while tokenized finance could improve efficiency, it may also introduce new forms of systemic risk capable of amplifying future financial crises.

As blockchain infrastructure becomes increasingly integrated into traditional finance, the debate is shifting from:

“Will tokenization happen?”

to:

“Can the global financial system safely handle it?”

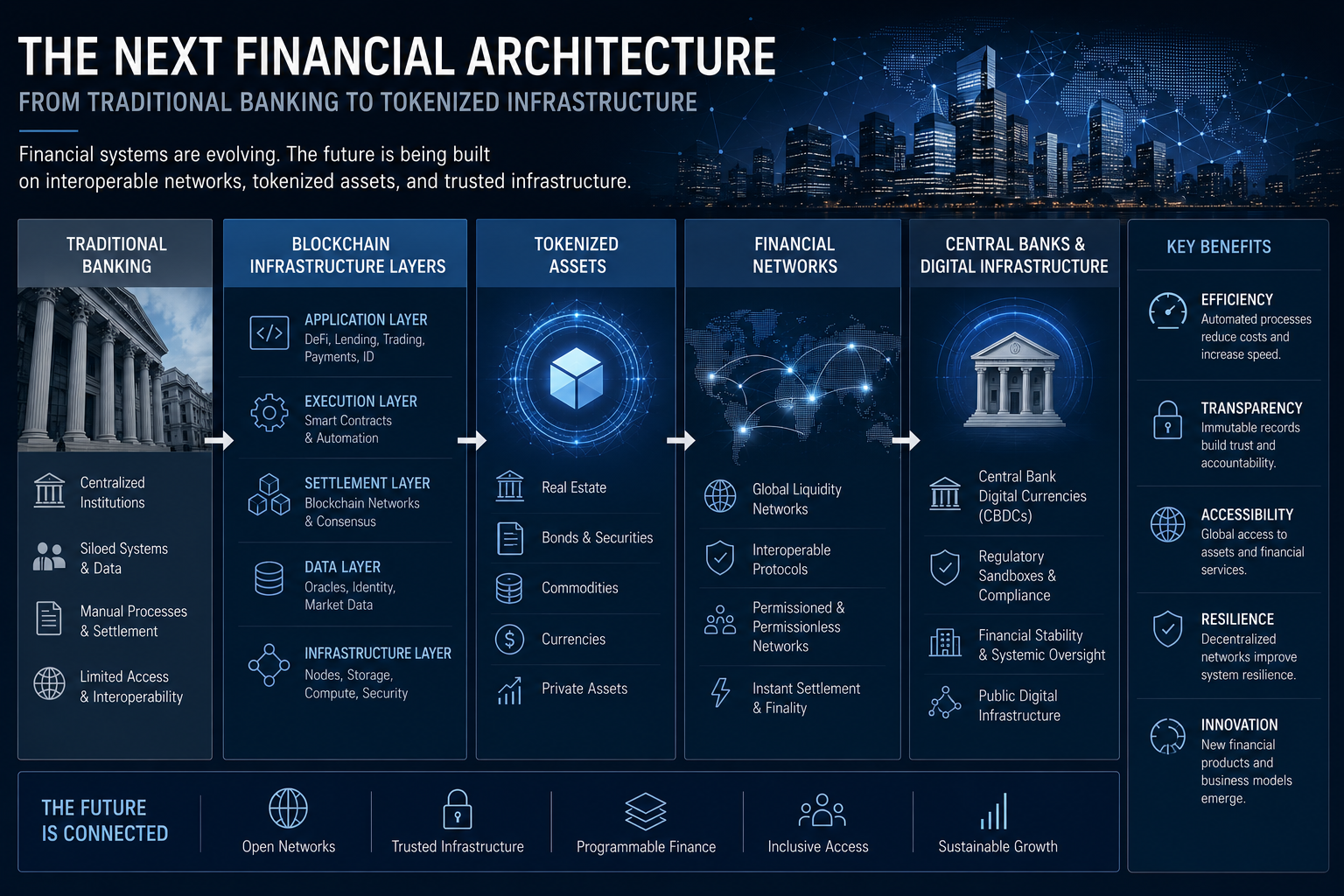

What Is Tokenized Finance?

Tokenized finance refers to the process of converting traditional financial assets into blockchain-based digital tokens.

Instead of relying on conventional financial infrastructure and settlement systems, tokenized assets can move across blockchain networks with near-instant settlement and programmable ownership rules.

Assets that can potentially be tokenized include:

- stocks

- government bonds

- real estate

- private equity

- commodities

- money market funds

- treasury products

This process allows financial assets to become:

- digitally transferable

- programmable

- globally accessible

- interoperable with blockchain infrastructure

Many institutions view tokenization as a major step toward the modernization of financial markets.

Growing discussions around institutional blockchain adoption are already accelerating tokenization research and infrastructure development globally:

Why Financial Institutions Are Interested in Tokenization

Traditional financial infrastructure often suffers from:

- slow settlement systems

- fragmented markets

- operational inefficiencies

- expensive intermediaries

- limited market accessibility

Tokenization promises to improve many of these limitations.

Potential advantages include:

- faster settlement

- lower operational costs

- 24/7 markets

- programmable transactions

- fractional ownership

- global accessibility

Large financial firms including BlackRock, JPMorgan, and major exchanges are increasingly exploring tokenized asset infrastructure.

Supporters believe blockchain-based systems could eventually modernize:

- securities trading

- cross-border payments

- collateral management

- treasury operations

- settlement infrastructure

However, speed and automation may also introduce new vulnerabilities.

Why the IMF Is Concerned About Tokenized Finance

The IMF has warned that some of the same features making tokenization attractive could also create systemic financial risks.

Traditional financial systems often include delays between transaction execution and final settlement.

While these delays are frequently criticized as inefficient, they also provide:

- liquidity management time

- regulatory oversight windows

- intervention opportunities

- exposure netting mechanisms

Tokenized systems operate very differently.

Blockchain transactions can settle almost instantly, removing many of the timing buffers used by traditional financial systems during periods of market stress.

The IMF argues that this could make financial crises:

- faster

- more automated

- harder to contain

- more globally interconnected

In highly automated systems, market instability could spread rapidly before regulators or institutions have sufficient time to intervene.

Instant Settlement Could Accelerate Market Crashes

One of the biggest concerns surrounding tokenized finance is the impact of real-time settlement systems.

In traditional finance:

- settlements may take days

- liquidity can be injected gradually

- exposures can be netted

- emergency coordination is possible

Blockchain-based financial systems often operate continuously without these delays.

This creates the possibility of:

- automated liquidations

- rapid collateral calls

- algorithmic sell-offs

- cascading market failures

Smart contracts executing automatically during periods of extreme volatility could potentially amplify market instability rather than reduce it.

The broader Web3 ecosystem has already experienced several examples of automated market stress events linked to DeFi security risks and smart contract liquidations:

These events demonstrate how automation can sometimes accelerate financial instability instead of slowing it down.

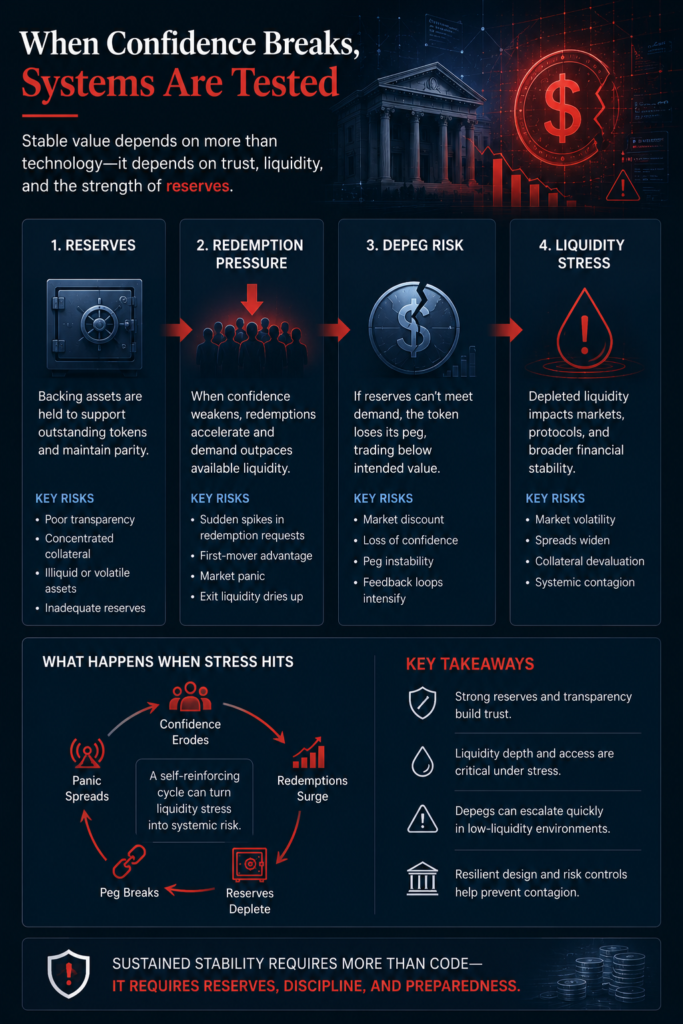

Stablecoins Could Become a Major Structural Risk

Stablecoins are expected to play a central role in tokenized financial systems.

They are often used as:

- settlement assets

- liquidity tools

- collateral instruments

- trading pairs

- payment rails

However, stablecoins also introduce unique risks.

Their stability depends heavily on:

- reserve quality

- liquidity access

- redemption confidence

- market trust

During periods of market stress, large-scale redemption requests could create pressure similar to traditional bank runs.

Even fully collateralized stablecoins may face challenges if reserves become illiquid or market panic spreads rapidly.

The collapse of confidence in major stablecoins could trigger wider disruptions across blockchain-based financial systems.

This is one reason why regulators and central banks are increasingly examining how stablecoin systems interact with broader financial infrastructure.

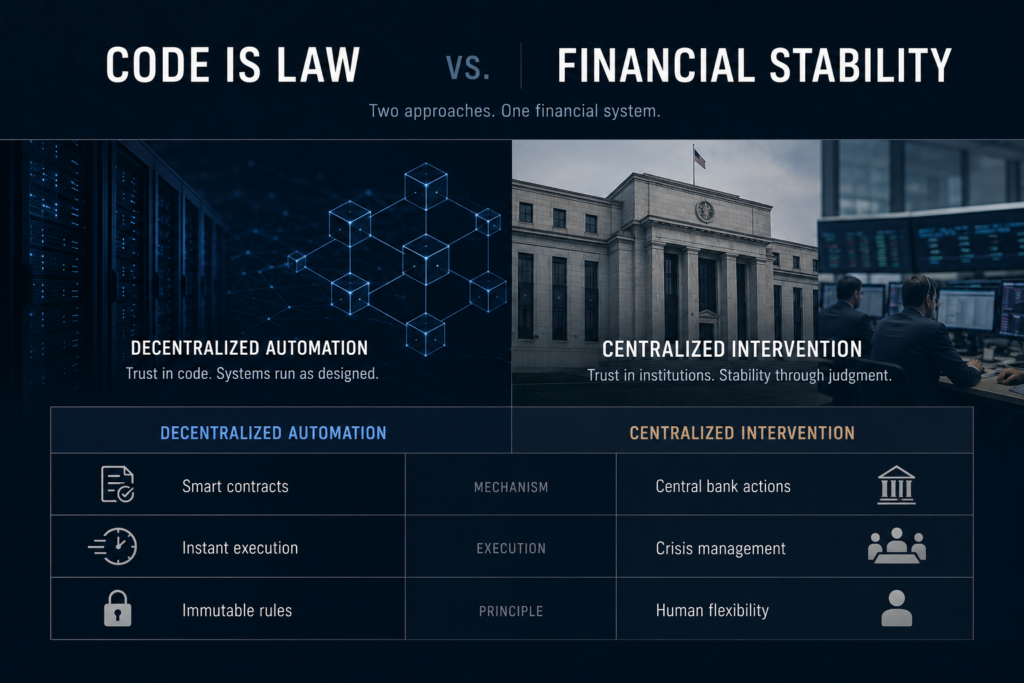

“Code Is Law” vs Financial Stability

One of the most important debates surrounding tokenized finance centers around automation.

Many decentralized systems operate according to the principle that:

“Code is law.”

In these systems:

- smart contracts execute automatically

- rules cannot easily be overridden

- transactions finalize without centralized control

While this increases efficiency and reduces intermediary dependence, it also removes flexibility during emergencies.

Traditional financial systems often rely on:

- central bank intervention

- emergency liquidity support

- market halts

- regulatory coordination

These mechanisms help slow panic during crises.

The IMF argues that fully automated financial infrastructure may struggle to handle extreme systemic stress without human oversight mechanisms.

As blockchain infrastructure evolves, the challenge will likely involve balancing:

- decentralization

- automation

- financial stability

- institutional safeguards

Why Governments and Central Banks Are Paying Attention

Tokenization is no longer limited to crypto-native projects.

Governments and central banks worldwide are increasingly exploring:

- central bank digital currencies (CBDCs)

- tokenized treasuries

- blockchain settlement systems

- regulated digital assets

- institutional blockchain infrastructure

This growing interest reflects broader concerns around:

- payment system modernization

- financial competitiveness

- digital infrastructure resilience

- monetary control

At the same time, governments are also evaluating how blockchain systems interact with national cybersecurity and strategic infrastructure priorities.

Growing discussions surrounding Bitcoin’s role in cybersecurity infrastructure show how decentralized networks are increasingly entering national-level policy conversations:

Why Smart Contract Security Matters in Tokenized Finance

As tokenized systems become more complex, smart contract security becomes increasingly critical.

Financial infrastructure built on blockchain systems depends heavily on:

- secure code execution

- reliable automation

- protocol integrity

- vulnerability prevention

Even small coding flaws can create significant financial risks when billions of dollars are involved.

Modern smart contract security systems are increasingly integrating AI-assisted auditing and automated vulnerability detection to improve infrastructure resilience:

Without strong security standards, tokenized financial infrastructure may remain vulnerable to:

- exploits

- liquidity failures

- manipulation

- systemic contagion

The Future of Tokenized Financial Infrastructure

Despite regulatory concerns, tokenization adoption continues accelerating.

Major institutions are already experimenting with:

- tokenized bonds

- blockchain settlements

- on-chain treasury products

- tokenized real estate

- digital securities

If adoption continues expanding, tokenized systems could eventually reshape:

- global settlement infrastructure

- banking systems

- collateral markets

- capital formation

- cross-border finance

At the same time, the success of tokenized finance will likely depend on:

- regulatory clarity

- infrastructure resilience

- liquidity management

- cybersecurity standards

- institutional trust

The long-term challenge will not simply involve technological innovation.

It will involve ensuring that highly automated financial systems remain stable during periods of global stress.

Final Thoughts

Tokenized finance represents one of the most significant transformations currently occurring within global financial infrastructure.

The technology promises:

- faster markets

- lower costs

- greater efficiency

- increased accessibility

- programmable financial systems

However, these same advantages may also introduce new systemic vulnerabilities capable of accelerating financial instability during crises.

The IMF’s concerns highlight an increasingly important reality:

financial systems built on blockchain infrastructure must balance innovation with resilience.

As institutions, governments, and blockchain companies continue pushing tokenization forward, the future of finance may ultimately depend on how effectively these systems manage:

- automation

- liquidity

- regulation

- security

- market stability

Tokenized finance is no longer a niche blockchain experiment.

It is becoming part of the broader evolution of global financial infrastructure.

FAQ

What is tokenized finance?

Tokenized finance refers to converting traditional financial assets into blockchain-based digital tokens that can move across decentralized infrastructure.

Why are institutions interested in tokenization?

Institutions are exploring tokenization to improve settlement speed, liquidity, operational efficiency, and financial accessibility.

Why is the IMF concerned about tokenized finance?

The IMF believes highly automated and instantly settled blockchain systems could amplify financial crises and reduce intervention opportunities during market stress.

What role do stablecoins play in tokenized finance?

Stablecoins are commonly used for settlement, liquidity, and collateral within tokenized financial systems.

What are the biggest risks in tokenized finance?

Major risks include smart contract vulnerabilities, stablecoin instability, regulatory uncertainty, automated liquidations, and systemic financial contagion.